“Fully-collateralized commodity futures have historically offered the same return and Sharpe ratio as equities.

While the risk premium on commodity futures is essentially the same as equities, commodity futures returns are negatively correlated with equity returns and bond returns. The negative correlation between commodity futures and the other asset classes is due, in significant part, to different behavior over the business cycle.

In addition, commodity futures are positively correlated with inflation, unexpected inflation, and changes in expected inflation.”

“Facts and Fantasies about Commodity futures” Yale International Centre for Finance (2004)

People have traded commodities for millennia, long before the advent of financial exchanges. Amsterdam, of tulip mania notoriety, was one of the earliest formal commodities exchanges in the 16th century. Osaka, Japan, was the first to trade commodity futures (rice) in the 17th century. A hundred years’ later formal commodity futures exchanges began trading in the US (agricultural contracts on the US Chicago Board of Trade in 1848) and in England (metals on the London Metals Exchange in 1877).

The rationale for, and impact of, the integration of commodities as an asset class into a diversified multi-asset investment portfolio is reviewed in this document. Briefly, commodities’ characteristics of (i) positive correlation with inflation (ii) non-correlation with traditional financial assets and (iii) their ability to contribute absolute returns justify their inclusion in a diversified portfolio. These characteristics improve the risk adjusted returns of almost every type of investment portfolio, increasing investors’ confidence in achieving their strategic investment goals. The quantum of a commodity allocation may be established using conventional portfolio construction techniques. We illustrate what an optimal allocation might be and its effects on the relevant portfolios’ return characteristics.

All asset classes do well at times, but none do well all the time. Bonds appear to have ended their thirty-year bull market and, after a remarkable post-Covid 19 rally, equities are again at record highs. In contrast, after a decade-long bear market in which commodity indices have fallen 75%, commodities appear to be the only cheap asset class. Further with politics worldwide becoming more populist, economies worldwide appear to be on the cusp of the greatest peacetime fiscal stimulus in history. This will undoubtedly increase the demand for commodities and the reflation trade is on everyone’s lips, if not their portfolios. Finally, equity investors are tactically rotating from growth to value. It is an opportune time for investors to re-examine their strategic asset allocation with a view to adding or increasing their allocation to commodities.

The inclusion of commodities can provide the following characteristics to any investment portfolio: firstly, commodities have inherent inflation hedging properties given their role as an input in most economic production. Secondly, commodities have consistently low correlations with other traditional asset classes which improves the level of diversification in a portfolio. The fact that commodities have fundamentally different risk drivers to traditional asset classes (e.g. weather for agricultural and politics for energy commodities) means that an allocation to commodities can consistently enhance these portfolio diversification levels, particularly in times of crisis (when correlations between the traditional asset classes increase). Finally, investors can earn consistent absolute returns from commodities by the application of robust risk management techniques to a diversified portfolio, rather than buying-and holding commodity beta. For non-dollar investors, there is also a potential currency hedge benefit to holding commodities.

Commodities as an inflation hedge

“First they deny that inflation is a problem. Then they say it’s only due to specific transitory factors. Then finally they say it’s not really that big a problem after all.”

Larry Summers, former US Treasury Secretary, May 2021

“We’ve been fighting inflation that’s too low and interest rates that are too low now for a decade. We want them to go back to a normal interest rate environment, and if this helps a little bit to alleviate things then that’s not a bad thing – that’s a good thing.”

Janet Yellen, Former US Federal Reserve Chair and current US Treasury Secretary, June 2021

“China’s Manufacturing Prices Skyrocket — Biggest increase in nearly 13 years puts pressure on Beijing. Today’s data showed that the pressure of soaring raw-material prices is pretty heavy for industrial firms and such pressure is now passed through to downstream firms in an accelerated way. Industrial inflation pressure will likely remain and pose additional risks to economic growth.”

Bloomberg World News 10 June 2021.

As commodities are typically inputs into the production of most goods, some of the changes in the inflation level can be explained by the changes in commodity prices. The oil price shock of the 1970’s was the most extreme example of this effect. The fundamental nature of the relationship between the price of inputs and the price of outputs makes this positive relationship between the two a reliable one (although there will be some variability in terms of the lagged effects of cost-price increases filtering through to consumer prices changes).

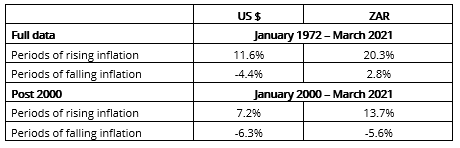

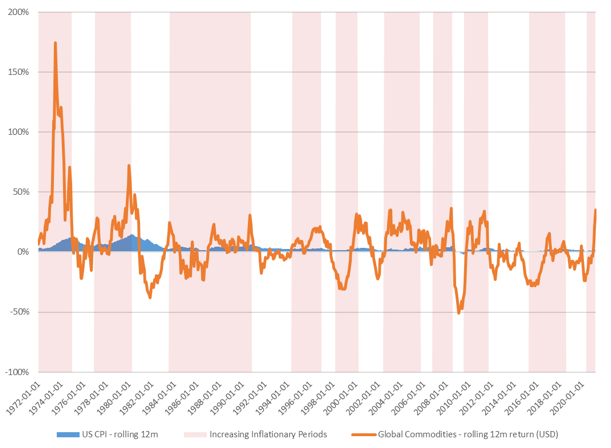

A review of the performance of commodities (as proxied by the Bloomberg Commodities Index – BCOM) in increasing inflationary periods in clearly shows the positive relationship. The relationship over time for the United States (in USD) is summarized in Figure 1 below. The periods of rising inflation are illustrated by the shaded pink vertical bars and the levels of CPI increases (i.e. inflation) and commodity returns are calculated over rolling 12-month periods. The average annualized commodity returns over the periods of rising inflation are summarized in the table below, both for the entire period for which data is available and a common period (since 2000 – where available):Average 12-month commodity index returns during:

Figure 1. US Inflation Experience and Commodity Returns (both rolling 12m values in USD)

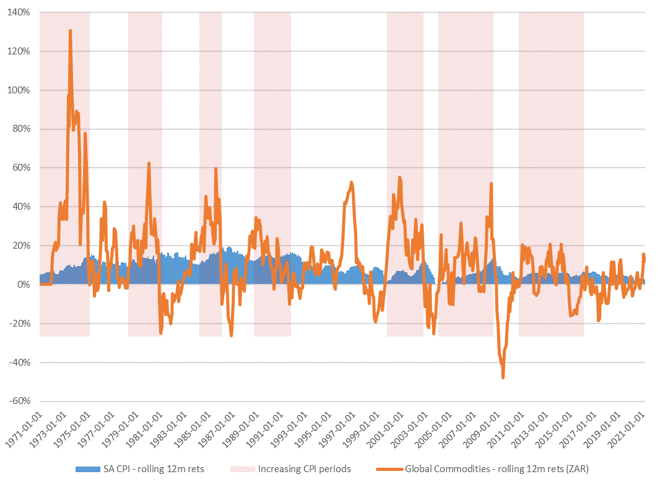

Figure 2. South African Inflation Experience and Commodity Returns (both rolling 12m values in ZAR)

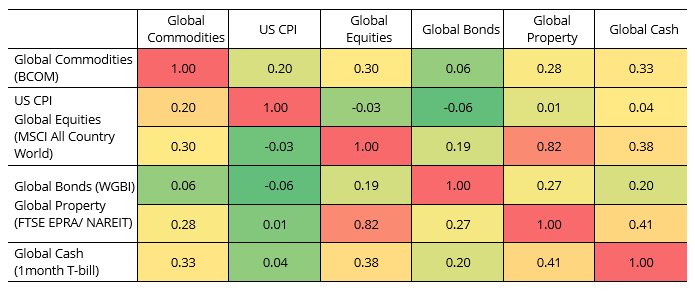

Commodities as an additional source of diversification

Diversification is an important element of portfolio risk management. The greater the range of uncorrelated assets with positive returns included in a portfolio, the better the overall risk adjusted performance. As is illustrated in the tables below, commodities have excellent low correlations with other traditional asset classes. In addition, the differing natures of their underlying return drivers should provide investors with confidence that these correlations will remain low or negative into the future – they really are very different investments indeed.

It is further worth noting that both global bonds (WGBI) and global equities (MSCI World) have negative correlations with rising US CPI.

Table 2. Correlations of monthly returns (in USD) for the period 1985 –2021

Commodities and absolute returns

“Agricultural commodity prices are driven by the weather, energy prices by politics and metal prices by economics.”

Sandra Gordon (Coherent Capital Management consulting economist, 2013)

In an environment where commodity prices cycle through bull and bear markets, the cross-sectional volatility between the broad commodity sectors of agriculture, energy and metals and their underlying individual constituents provides rich scope for harvesting alpha in excess of that on offer from the asset class beta.

Given this price cyclicality, the greatest return available from investment in the asset class is available from an investment strategy that is able to go both long and short. However this does typically result in higher volatility of returns, and many mandates do not permit investment in such strategies.

A long only, ungeared investment strategy is also perfectly feasible. It is able to deliver real returns at essentially the same risk as equities (as per the Yale quote on page 1), with the additional benefit of low correlation with the traditional asset classes.

Our next article will look into why you should invest in commodities now.

Author: Andy Pfaff

Download a PDF version of this article.

![]()